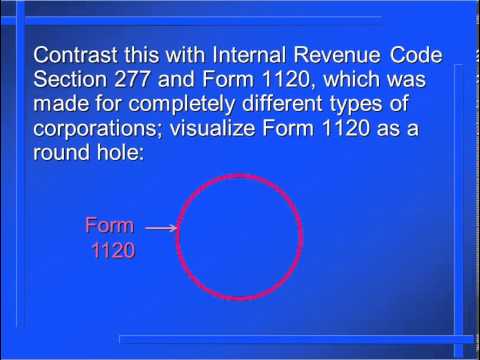

Welcome to our presentation on homeowners association taxation. This presentation is focused on understanding the differences between Form 1120 H and Form 1120, with special emphasis on the risk inherent in Form 1120. The homeowners association industry area of taxation is really confusing for a lot of people. It is far more complex than it looks like, and that's because this is the only entity in the entire universe of tax law that has the option of filing two different tax returns and making an annual election to do so. Form 1120 H is designed specifically for homeowners associations and is a one-page form, but with a thirty percent tax rate. Form 1120 was designed for for-profit corporations and was not designed specifically for this industry, but it carries only a fifteen percent tax rate. That's why it is so popular. The other reason that tax law is so confusing for this industry is that it's simply not codified. What that means is it simply doesn't exist in one place. Somebody who wants to practice in this area needs to have a great depth and breadth of tax knowledge to understand all of the possible code sections, Treasury regulations, court cases, revenue rulings, and private letter rulings that could apply to an association. It's really helpful to try and visualize these things just to grasp the major concepts. The easiest way to look at this is to visualize your association as a square peg. Next, visualize Form 1120 H as a square hole. It looks basically the same shape because Congress created this tax law specifically for your association. As you could guess, your association fits very nicely as your square peg into that square hole. It was made to do so. Contrast this with Form 1120. Remember, it was made for for-profit corporations....

Award-winning PDF software

Video instructions and help with filling out and completing Fill Form 1120 Schedule M 3 Attributable